A star is struck

The first fund I bought 5 years ago when I had a windfall was Neil Woodford’s flagship Equity Income Fund. Everyone in finance had heard of his brilliant stewardship of Investco funds when he out-performed the market and avoided the dot.com bubble.

However, when I had lunch soon after its acquisition with the mother of my godchild, a conservative but vastly experienced fund manager, she warned me against him.

However, when I had lunch soon after its acquisition with the mother of my godchild, a conservative but vastly experienced fund manager, she warned me against him.

Undeterred, as I’m not terribly good at taking advice from women, I held my investment and bought other of his funds. In October of last year when the market reached (peaked in my view) at 7500.

I read the financial pages carefully and I can’t recalling advice to mark down the flagship as a sell. There are 3 categories – sell, buy or hold – though the excellent financial pages of the Mail On Sunday will often recommend a partial sell.

With ISA-finding a priority, I intended to sell the Equity Income Fund. At a weekend 10 days ago with the family of my godson, I thanked his mother for her hospitality and for the Woodford tip.

Then I realised I did not get round to selling the residue and would and did so on Monday. I was surprised as it is an investment trust, a supposedly liquid fund, that the sale did not proceed but was marked as ‘pending’.

Then I realised I did not get round to selling the residue and would and did so on Monday. I was surprised as it is an investment trust, a supposedly liquid fund, that the sale did not proceed but was marked as ‘pending’.

All was clarified when Woodford suspended dealing on the fund for an definite period as there was a run on it after Kent Council placed a £250,000 order for sale.

Since so many of his investments were illiquid in private companies he could only sell off the quoted ones. In Kier, Provident and Purple Bricks he hardly enhanced his reputation as a stock picker. An investment trust has two attractions: because its value goes up and down you can buy at a discount when the latter happens. Secondly, it is supposed to be liquid. Woodford got round this by holding shares quoted on the Guernsey Stock exchange.

In these situations the reaction of the fund manager is crucial.

In these situations the reaction of the fund manager is crucial.

He released a video which did not placate those stuck in his fund. He should have used some of his £49m he has taken in dividends and £100,000 daily fees would be allocated to shore up the fund to make it more liquid and crucially waive all management fees.

He did none of these.

His reputation is in tatters and at 59 can he make a comeback?

His reputation is in tatters and at 59 can he make a comeback?

I think not.

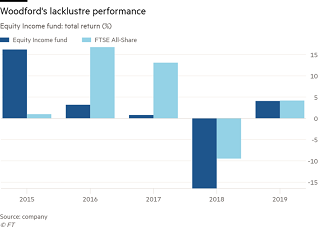

Those who know about these things observe that Nick Train and Terry Smith have done better the past few years in outperforming the market.

Nor have financial advisers emerged well out of this. Hargreaves Lansdowne only dropped the fund from its influential top 50 funds after it was gated. The Government, as ever, have acted after the horse has bolted.

The Financial Conduct Authority will be hauled over the coals and more stringent liquidity regulations applied but this will be of little comfort to the many pensioners who thought their money was safe with Woodford flagship fund.